Mastering Time Collection Forecasting: From ARIMA to LSTM

Mastering Time Collection Forecasting: From ARIMA to LSTM

Picture by Editor | Midjourney

Introduction

Time sequence forecasting is a statistical method used to investigate historic information factors and predict future values based mostly on temporal patterns. This methodology is especially priceless in domains the place understanding tendencies, seasonality, and cyclical patterns drives crucial enterprise selections and strategic planning. From predicting inventory market fluctuations to forecasting vitality demand spikes, correct time sequence evaluation helps organizations optimize stock, allocate assets effectively, and mitigate operational dangers. Fashionable approaches mix conventional statistical strategies with machine studying to deal with each linear relationships and complicated nonlinear patterns in temporal information.

On this article, we’ll discover three primary strategies for forecasting:

- Autoregressive Built-in Transferring Common (ARIMA): A easy and well-liked methodology that makes use of previous values to make predictions

- Exponential Smoothing Time Collection (ETS): This methodology seems at tendencies and patterns over time to present higher forecasts

- Lengthy Quick-Time period Reminiscence (LSTM): A extra superior methodology that makes use of deep studying to grasp advanced information patterns

Preparation

First, we import the required libraries.

|

# Import needed libraries import pandas as pd import numpy as np import matplotlib.pyplot as plt from statsmodels.tsa.arima.mannequin import ARIMA from statsmodels.tsa.stattools import adfuller from statsmodels.tsa.holtwinters import ExponentialSmoothing from prophet import Prophet from sklearn.model_selection import train_test_split from sklearn.preprocessing import MinMaxScaler from keras.fashions import Sequential from keras.layers import LSTM, Dense, Enter |

Then, we load the time sequence and look at its first few rows.

|

# Load your dataset df = pd.read_csv(‘timeseries.csv’, parse_dates=[‘Date’], index_col=‘Date’) df.head() |

1. Autoregressive Built-in Transferring Common (ARIMA)

ARIMA is a widely known methodology used to foretell future values in a time sequence. It combines three elements:

- AutoRegressive (AR): The connection between an remark and a variety of lagged observations

- Built-in (I): The differencing of uncooked observations to permit for the time sequence to develop into stationary

- Transferring Common (MA): The connection reveals how an remark differs from the anticipated worth in a shifting common mannequin utilizing previous information

We use the Augmented Dickey-Fuller (ADF) check to test if our information stays the identical over time. We have a look at the p-value from this check. If the p-value is 0.05 or decrease, it means our information is secure.

|

# ADF Take a look at to test for stationarity outcome = adfuller(df[‘Price’])

print(‘ADF Statistic:’, outcome[0]) print(‘p-value:’, outcome[1])

if outcome[1] > 0.05: print(“The sequence is non-stationary. Differencing is required.”) else: print(“The sequence is stationary.”) |

We carry out first-order differencing on the time sequence information to make it stationary.

|

# First-order differencing df[‘Differenced’] = df[‘Price’].diff()

# Drop lacking values ensuing from differencing df.dropna(inplace=True)

# Show the primary few rows of the differenced information print(df[[‘Price’, ‘Differenced’]].head()) |

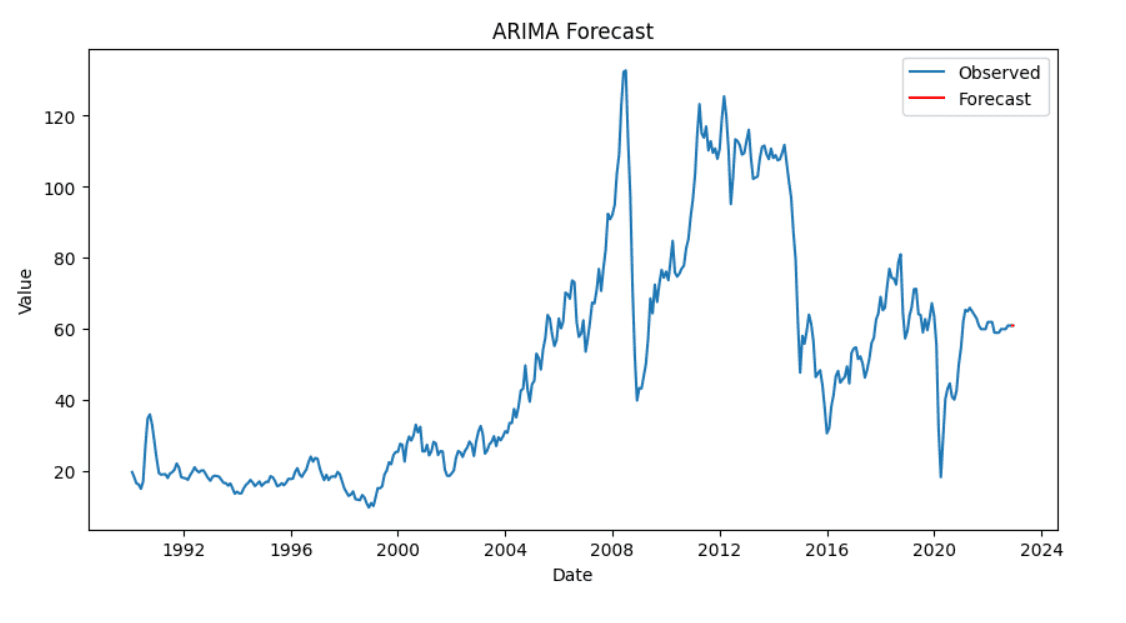

We create and match the ARIMA mannequin to our information. After becoming the mannequin, we forecast the long run values.

|

# Match the ARIMA mannequin mannequin = ARIMA(df[‘Price’], order=(1, 1, 1)) model_fit = mannequin.match()

# Forecasting subsequent steps forecast = model_fit.forecast(steps=10) |

Lastly, we visualize our outcomes to check the precise and predicted values.

|

# Plotting the outcomes plt.determine(figsize=(10, 5)) plt.plot(df[‘Price’], label=‘Noticed’) plt.plot(pd.date_range(df.index[–1], intervals=10, freq=‘D’), forecast, label=‘Forecast’, shade=‘purple’) plt.title(‘ARIMA Forecast’) plt.xlabel(‘Date’) plt.ylabel(‘Worth’) plt.legend() plt.present() |

2. Exponential Smoothing Time Collection (ETS)

Exponential smoothing is a technique used for time sequence forecasting. It contains three elements:

- Error (E): Represents the unpredictability or noise within the information

- Development (T): Reveals the long-term route of the information

- Seasonality (S): Captures repeating patterns or cycles within the information

We are going to use the Holt-Winters methodology for performing ETS. ETS helps us predict information that has each tendencies and seasons.

|

# Match the ETS mannequin (Exponential Smoothing) ets_model = ExponentialSmoothing(df[‘Price’], seasonal=‘add’, pattern=‘add’, seasonal_periods=12) ets_fit = ets_model.match() |

We generate forecasts for a specified variety of intervals utilizing the fitted ETS mannequin.

|

# Forecasting the following 12 intervals forecast = ets_fit.forecast(steps=12) |

Then, we plot the noticed information together with the forecasted values to visualise the mannequin’s efficiency.

|

# Plot noticed and forecasted values plt.determine(figsize=(10, 6)) plt.plot(df, label=‘Noticed’) plt.plot(forecast, label=‘Forecast’, shade=‘purple’) plt.title(‘ETS Mannequin Forecast’) plt.xlabel(‘Date’) plt.ylabel(‘Worth’) plt.legend() plt.present() |

3. Lengthy Quick-Time period Reminiscence (LSTM)

LSTM is a kind of neural community that appears at information in a sequence. It’s good at remembering vital particulars for a very long time. This makes it helpful for predicting future values in time sequence information as a result of it might probably discover advanced patterns.

LSTM is delicate to scale of the information. So, we regulate the goal variable to verify all values are between 0 and 1. This course of is known as normalization.

|

# Extract the values of the goal column information = df[‘Price’].values information = information.reshape(–1, 1)

# Normalize the information scaler = MinMaxScaler(feature_range=(0, 1)) scaled_data = scaler.fit_transform(information)

# Show the primary few scaled values print(scaled_data[:5]) |

LSTM expects enter within the type of sequences. Right here, we’ll cut up the time sequence information into sequences (X) and their corresponding subsequent worth (y).

|

# Create a operate to transform information into sequences for LSTM def create_sequences(information, time_steps=60): X, y = [], [] for i in vary(len(information) – time_steps): X.append(information[i:i+time_steps, 0]) y.append(information[i+time_steps, 0]) return np.array(X), np.array(y)

# Use 60 time steps to foretell the following worth time_steps = 60 X, y = create_sequences(scaled_data, time_steps)

# Reshape X for LSTM enter X = X.reshape(X.form[0], X.form[1], 1) |

We cut up the information into coaching and check units.

|

# Cut up the information into coaching and check units (80% practice, 20% check) train_size = int(len(X) * 0.8) X_train, X_test = X[:train_size], X[train_size:] y_train, y_test = y[:train_size], y[train_size:] |

We are going to now construct the LSTM mannequin utilizing Keras. Then, we’ll compile it utilizing the Adam optimizer and imply squared error loss.

|

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 |

from keras.fashions import Sequential from keras.layers import LSTM, Dense, Enter

# Initialize the Sequential mannequin mannequin = Sequential()

# Outline the enter layer mannequin.add(Enter(form=(time_steps, 1)))

# Add the LSTM layer mannequin.add(LSTM(50, return_sequences=False))

# Add a Dense layer for output mannequin.add(Dense(1))

# Compile the mannequin mannequin.compile(optimizer=‘adam’, loss=‘mean_squared_error’) |

We practice the mannequin utilizing the coaching information. We additionally consider the mannequin’s efficiency on the check information.

|

# Practice the mannequin on the coaching information historical past = mannequin.match(X_train, y_train, epochs=20, batch_size=32, validation_data=(X_test, y_test)) |

After we practice the mannequin, we’ll use it to foretell the outcomes on the check information.

|

# Make predictions on the check information y_pred = mannequin.predict(X_test)

# Inverse rework the predictions and precise values to authentic scale y_pred_rescaled = scaler.inverse_transform(y_pred) y_test_rescaled = scaler.inverse_transform(y_test.reshape(–1, 1))

# Show the primary few predicted and precise values print(y_pred_rescaled[:5]) print(y_test_rescaled[:5]) |

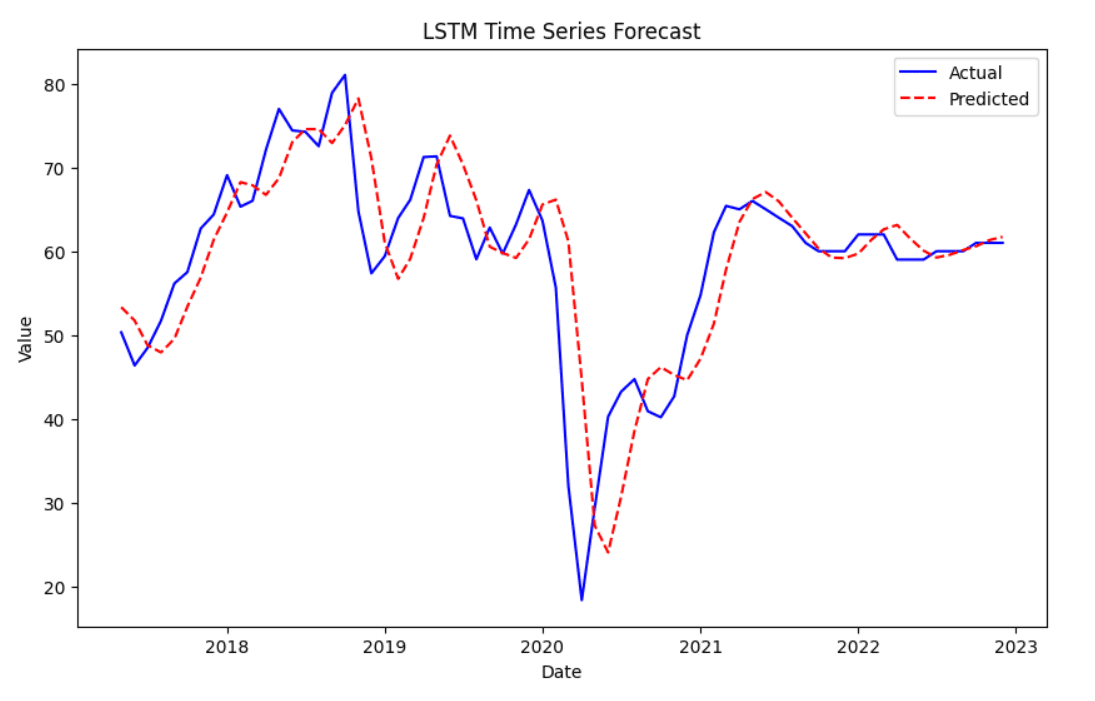

Lastly, we will visualize the anticipated values towards the precise values. The precise values are proven in blue, whereas the anticipated values are in purple with a dashed line.

|

# Plot the precise vs predicted values plt.determine(figsize=(10,6)) plt.plot(df.index[–len(y_test_rescaled):], y_test_rescaled, label=‘Precise’, shade=‘blue’) plt.plot(df.index[–len(y_test_rescaled):], y_pred_rescaled, label=‘Predicted’, shade=‘purple’, linestyle=‘dashed’) plt.title(‘LSTM Time Collection Forecast’) plt.xlabel(‘Date’) plt.ylabel(‘Worth’) plt.legend() plt.present() |

Wrapping Up

On this article, we explored time sequence forecasting utilizing completely different strategies.

We began with the ARIMA mannequin. First, we checked if the information was stationary, after which we fitted the mannequin.

Subsequent, we used Exponential Smoothing to seek out tendencies and seasonality within the information. This helps us see patterns and make higher forecasts.

Lastly, we constructed a Lengthy Quick-Time period Reminiscence mannequin. This mannequin can study sophisticated patterns within the information. We scaled the information, created sequences, and skilled the LSTM to make predictions.

Hopefully this information has been of use to you in overlaying these time sequence forecasting strategies.