Predicting Fraud with Autoencoders and Keras

Overview

On this publish we’ll prepare an autoencoder to detect bank card fraud. We can even display learn how to prepare Keras fashions within the cloud utilizing CloudML.

The idea of our mannequin would be the Kaggle Credit Card Fraud Detection dataset, which was collected throughout a analysis collaboration of Worldline and the Machine Learning Group of ULB (Université Libre de Bruxelles) on huge information mining and fraud detection.

The dataset incorporates bank card transactions by European cardholders remodeled a two day interval in September 2013. There are 492 frauds out of 284,807 transactions. The dataset is extremely unbalanced, the constructive class (frauds) account for less than 0.172% of all transactions.

Studying the information

After downloading the information from Kaggle, you’ll be able to learn it in to R with read_csv():

The enter variables encompass solely numerical values that are the results of a PCA transformation. In an effort to protect confidentiality, no extra details about the unique options was offered. The options V1, …, V28 have been obtained with PCA. There are nevertheless 2 options (Time and Quantity) that weren’t remodeled.

Time is the seconds elapsed between every transaction and the primary transaction within the dataset. Quantity is the transaction quantity and could possibly be used for cost-sensitive studying. The Class variable takes worth 1 in case of fraud and 0 in any other case.

Autoencoders

Since solely 0.172% of the observations are frauds, we’ve a extremely unbalanced classification downside. With this sort of downside, conventional classification approaches normally don’t work very nicely as a result of we’ve solely a really small pattern of the rarer class.

An autoencoder is a neural community that’s used to study a illustration (encoding) for a set of information, usually for the aim of dimensionality discount. For this downside we’ll prepare an autoencoder to encode non-fraud observations from our coaching set. Since frauds are presupposed to have a unique distribution then regular transactions, we count on that our autoencoder could have greater reconstruction errors on frauds then on regular transactions. Which means we will use the reconstruction error as a amount that signifies if a transaction is fraudulent or not.

If you wish to study extra about autoencoders, a very good place to begin is that this video from Larochelle on YouTube and Chapter 14 from the Deep Learning ebook by Goodfellow et al.

Visualization

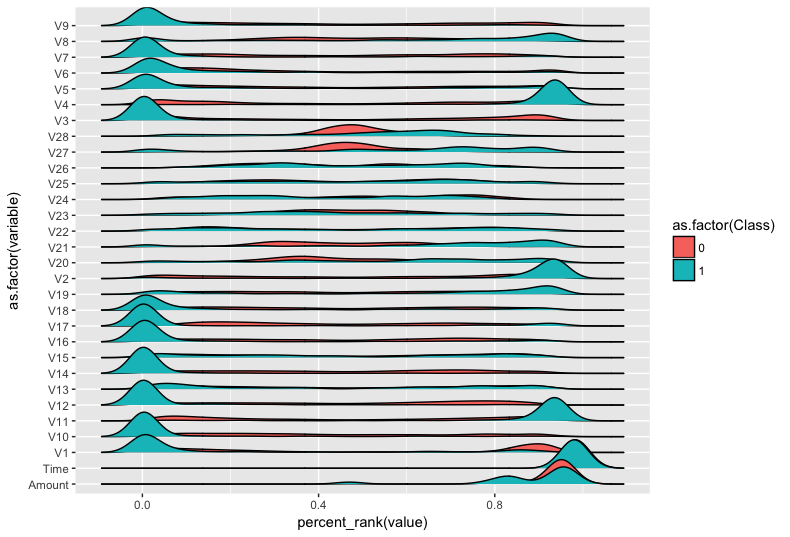

For an autoencoder to work nicely we’ve a robust preliminary assumption: that the distribution of variables for regular transactions is completely different from the distribution for fraudulent ones. Let’s make some plots to confirm this. Variables have been remodeled to a [0,1] interval for plotting.

We will see that distributions of variables for fraudulent transactions are very completely different then from regular ones, aside from the Time variable, which appears to have the very same distribution.

Preprocessing

Earlier than the modeling steps we have to do some preprocessing. We are going to cut up the dataset into prepare and check units after which we’ll Min-max normalize our information (that is accomplished as a result of neural networks work significantly better with small enter values). We can even take away the Time variable because it has the very same distribution for regular and fraudulent transactions.

Based mostly on the Time variable we’ll use the primary 200,000 observations for coaching and the remainder for testing. That is good apply as a result of when utilizing the mannequin we need to predict future frauds based mostly on transactions that occurred earlier than.

Now let’s work on normalization of inputs. We created 2 capabilities to assist us. The primary one will get descriptive statistics concerning the dataset which can be used for scaling. Then we’ve a operate to carry out the min-max scaling. It’s vital to notice that we utilized the identical normalization constants for coaching and check units.

library(purrr)

#' Will get descriptive statistics for each variable within the dataset.

get_desc <- operate(x) {

map(x, ~list(

min = min(.x),

max = max(.x),

imply = mean(.x),

sd = sd(.x)

))

}

#' Given a dataset and normalization constants it would create a min-max normalized

#' model of the dataset.

normalization_minmax <- operate(x, desc) {

map2_dfc(x, desc, ~(.x - .y$min)/(.y$max - .y$min))

}Now let’s create normalized variations of our datasets. We additionally remodeled our information frames to matrices since that is the format anticipated by Keras.

We are going to now outline our mannequin in Keras, a symmetric autoencoder with 4 dense layers.

___________________________________________________________________________________

Layer (sort) Output Form Param #

===================================================================================

dense_1 (Dense) (None, 15) 450

___________________________________________________________________________________

dense_2 (Dense) (None, 10) 160

___________________________________________________________________________________

dense_3 (Dense) (None, 15) 165

___________________________________________________________________________________

dense_4 (Dense) (None, 29) 464

===================================================================================

Whole params: 1,239

Trainable params: 1,239

Non-trainable params: 0

___________________________________________________________________________________We are going to then compile our mannequin, utilizing the imply squared error loss and the Adam optimizer for coaching.

mannequin %>% compile(

loss = "mean_squared_error",

optimizer = "adam"

)Coaching the mannequin

We will now prepare our mannequin utilizing the match() operate. Coaching the mannequin within reason quick (~ 14s per epoch on my laptop computer). We are going to solely feed to our mannequin the observations of regular (non-fraudulent) transactions.

We are going to use callback_model_checkpoint() in an effort to save our mannequin after every epoch. By passing the argument save_best_only = TRUE we’ll carry on disk solely the epoch with smallest loss worth on the check set.

We can even use callback_early_stopping() to cease coaching if the validation loss stops lowering for five epochs.

checkpoint <- callback_model_checkpoint(

filepath = "mannequin.hdf5",

save_best_only = TRUE,

interval = 1,

verbose = 1

)

early_stopping <- callback_early_stopping(persistence = 5)

mannequin %>% match(

x = x_train[y_train == 0,],

y = x_train[y_train == 0,],

epochs = 100,

batch_size = 32,

validation_data = list(x_test[y_test == 0,], x_test[y_test == 0,]),

callbacks = list(checkpoint, early_stopping)

)Practice on 199615 samples, validate on 84700 samples

Epoch 1/100

199615/199615 [==============================] - 17s 83us/step - loss: 0.0036 - val_loss: 6.8522e-04d from inf to 0.00069, saving mannequin to mannequin.hdf5

Epoch 2/100

199615/199615 [==============================] - 17s 86us/step - loss: 4.7817e-04 - val_loss: 4.7266e-04d from 0.00069 to 0.00047, saving mannequin to mannequin.hdf5

Epoch 3/100

199615/199615 [==============================] - 19s 94us/step - loss: 3.7753e-04 - val_loss: 4.2430e-04d from 0.00047 to 0.00042, saving mannequin to mannequin.hdf5

Epoch 4/100

199615/199615 [==============================] - 19s 94us/step - loss: 3.3937e-04 - val_loss: 4.0299e-04d from 0.00042 to 0.00040, saving mannequin to mannequin.hdf5

Epoch 5/100

199615/199615 [==============================] - 19s 94us/step - loss: 3.2259e-04 - val_loss: 4.0852e-04 enhance

Epoch 6/100

199615/199615 [==============================] - 18s 91us/step - loss: 3.1668e-04 - val_loss: 4.0746e-04 enhance

...After coaching we will get the ultimate loss for the check set through the use of the consider() fucntion.

loss <- consider(mannequin, x = x_test[y_test == 0,], y = x_test[y_test == 0,])

loss loss

0.0003534254 Tuning with CloudML

We could possibly get higher outcomes by tuning our mannequin hyperparameters. We will tune, for instance, the normalization operate, the training price, the activation capabilities and the dimensions of hidden layers. CloudML makes use of Bayesian optimization to tune hyperparameters of fashions as described in this blog post.

We will use the cloudml package to tune our mannequin, however first we have to put together our venture by making a training flag for every hyperparameter and a tuning.yml file that may inform CloudML what parameters we need to tune and the way.

The total script used for coaching on CloudML might be discovered at https://github.com/dfalbel/fraud-autoencoder-example. A very powerful modifications to the code have been including the coaching flags:

FLAGS <- flags(

flag_string("normalization", "minmax", "Certainly one of minmax, zscore"),

flag_string("activation", "relu", "Certainly one of relu, selu, tanh, sigmoid"),

flag_numeric("learning_rate", 0.001, "Optimizer Studying Charge"),

flag_integer("hidden_size", 15, "The hidden layer measurement")

)We then used the FLAGS variable contained in the script to drive the hyperparameters of the mannequin, for instance:

mannequin %>% compile(

optimizer = optimizer_adam(lr = FLAGS$learning_rate),

loss = 'mean_squared_error',

)We additionally created a tuning.yml file describing how hyperparameters ought to be diverse throughout coaching, in addition to what metric we wished to optimize (on this case it was the validation loss: val_loss).

tuning.yml

trainingInput:

scaleTier: CUSTOM

masterType: standard_gpu

hyperparameters:

aim: MINIMIZE

hyperparameterMetricTag: val_loss

maxTrials: 10

maxParallelTrials: 5

params:

- parameterName: normalization

sort: CATEGORICAL

categoricalValues: [zscore, minmax]

- parameterName: activation

sort: CATEGORICAL

categoricalValues: [relu, selu, tanh, sigmoid]

- parameterName: learning_rate

sort: DOUBLE

minValue: 0.000001

maxValue: 0.1

scaleType: UNIT_LOG_SCALE

- parameterName: hidden_size

sort: INTEGER

minValue: 5

maxValue: 50

scaleType: UNIT_LINEAR_SCALEWe describe the kind of machine we need to use (on this case a standard_gpu occasion), the metric we need to decrease whereas tuning, and the the utmost variety of trials (i.e. variety of combos of hyperparameters we need to check). We then specify how we need to fluctuate every hyperparameter throughout tuning.

You’ll be able to study extra concerning the tuning.yml file at the Tensorflow for R documentation and at Google’s official documentation on CloudML.

Now we’re able to ship the job to Google CloudML. We will do that by working:

library(cloudml)

cloudml_train("prepare.R", config = "tuning.yml")The cloudml package deal takes care of importing the dataset and putting in any R package deal dependencies required to run the script on CloudML. In case you are utilizing RStudio v1.1 or greater, it would additionally will let you monitor your job in a background terminal. You too can monitor your job utilizing the Google Cloud Console.

After the job is completed we will acquire the job outcomes with:

This may copy the recordsdata from the job with the most effective val_loss efficiency on CloudML to your native system and open a report summarizing the coaching run.

Since we used a callback to save lots of mannequin checkpoints throughout coaching, the mannequin file was additionally copied from Google CloudML. Information created throughout coaching are copied to the “runs” subdirectory of the working listing from which cloudml_train() is known as. You’ll be able to decide this listing for the newest run with:

[1] runs/cloudml_2018_01_23_221244595-03You too can checklist all earlier runs and their validation losses with:

ls_runs(order = metric_val_loss, lowering = FALSE) run_dir metric_loss metric_val_loss

1 runs/2017-12-09T21-01-11Z 0.2577 0.1482

2 runs/2017-12-09T21-00-11Z 0.2655 0.1505

3 runs/2017-12-09T19-59-44Z 0.2597 0.1402

4 runs/2017-12-09T19-56-48Z 0.2610 0.1459

Use View(ls_runs()) to view all columnsIn our case the job downloaded from CloudML was saved to runs/cloudml_2018_01_23_221244595-03/, so the saved mannequin file is offered at runs/cloudml_2018_01_23_221244595-03/mannequin.hdf5. We will now use our tuned mannequin to make predictions.

Making predictions

Now that we educated and tuned our mannequin we’re able to generate predictions with our autoencoder. We have an interest within the MSE for every remark and we count on that observations of fraudulent transactions could have greater MSE’s.

First, let’s load our mannequin.

mannequin <- load_model_hdf5("runs/cloudml_2018_01_23_221244595-03/mannequin.hdf5",

compile = FALSE)Now let’s calculate the MSE for the coaching and check set observations.

A great measure of mannequin efficiency in extremely unbalanced datasets is the Space Below the ROC Curve (AUC). AUC has a pleasant interpretation for this downside, it’s the likelihood {that a} fraudulent transaction could have greater MSE then a standard one. We will calculate this utilizing the Metrics package deal, which implements all kinds of widespread machine studying mannequin efficiency metrics.

[1] 0.9546814

[1] 0.9403554To make use of the mannequin in apply for making predictions we have to discover a threshold (ok) for the MSE, then if if (MSE > ok) we think about that transaction a fraud (in any other case we think about it regular). To outline this worth it’s helpful to take a look at precision and recall whereas various the brink (ok).

possible_k <- seq(0, 0.5, size.out = 100)

precision <- sapply(possible_k, operate(ok) {

predicted_class <- as.numeric(mse_test > ok)

sum(predicted_class == 1 & y_test == 1)/sum(predicted_class)

})

qplot(possible_k, precision, geom = "line")

+ labs(x = "Threshold", y = "Precision")

recall <- sapply(possible_k, operate(ok) {

predicted_class <- as.numeric(mse_test > ok)

sum(predicted_class == 1 & y_test == 1)/sum(y_test)

})

qplot(possible_k, recall, geom = "line")

+ labs(x = "Threshold", y = "Recall")

A great place to begin could be to decide on the brink with most precision however we might additionally base our choice on how a lot cash we would lose from fraudulent transactions.

Suppose every handbook verification of fraud prices us $1 but when we don’t confirm a transaction and it’s a fraud we’ll lose this transaction quantity. Let’s discover for every threshold worth how a lot cash we might lose.

cost_per_verification <- 1

lost_money <- sapply(possible_k, operate(ok) {

predicted_class <- as.numeric(mse_test > ok)

sum(cost_per_verification * predicted_class + (predicted_class == 0) * y_test * df_test$Quantity)

})

qplot(possible_k, lost_money, geom = "line") + labs(x = "Threshold", y = "Misplaced Cash")

We will discover the most effective threshold on this case with:

[1] 0.005050505If we would have liked to manually confirm all frauds, it might value us ~$13,000. Utilizing our mannequin we will scale back this to ~$2,500.